The Global State of Gaming in 2026: The Battle for Attention

Now halfway through 2026, finalized data confirms that the global gaming market successfully recalibrated last year, reaching a total 2025 valuation of $197 billion (+7.5% YoY).

Mobile gaming alone rebounded to $108.4 billion, driven by a stabilized post-pandemic correction and a surge in high-value monetization.[1]

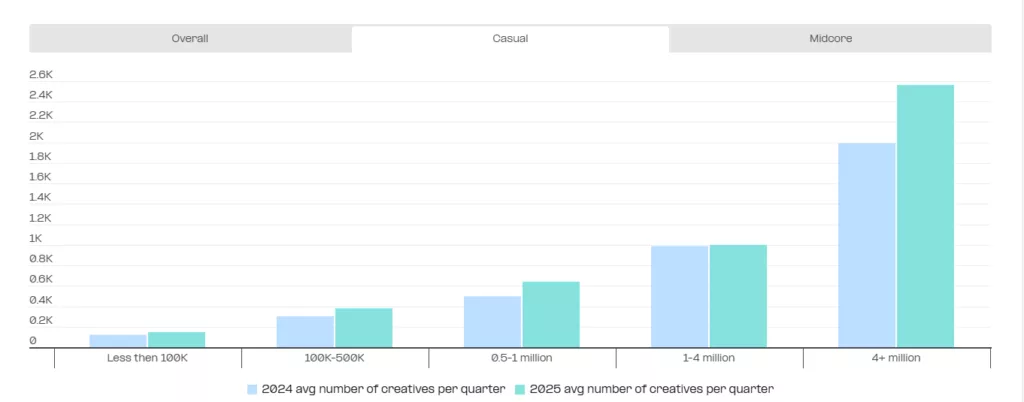

However, the defining narrative of the year was not about production—generative AI has made creating content easier than ever—but about attention. With top-tier publishers now producing ~2,600 creative variations per quarter (+30% YoY) to fight ad fatigue, the barrier to entry has shifted from development to discovery [2].

As noted by recent industry reports on mobile attribution, converting attention requires deep alignment with user expectations: “Winning opt-in remains a product and experience problem, not a market trend”.[3]

1. Global Heatmap: The Great Bifurcation

Regional Gaming Trends

The 2025 data reveals a sharp divide between where money is made and where players are acquired. The market has split into high-value “Fortresses” and high-velocity “Hot Zones.”

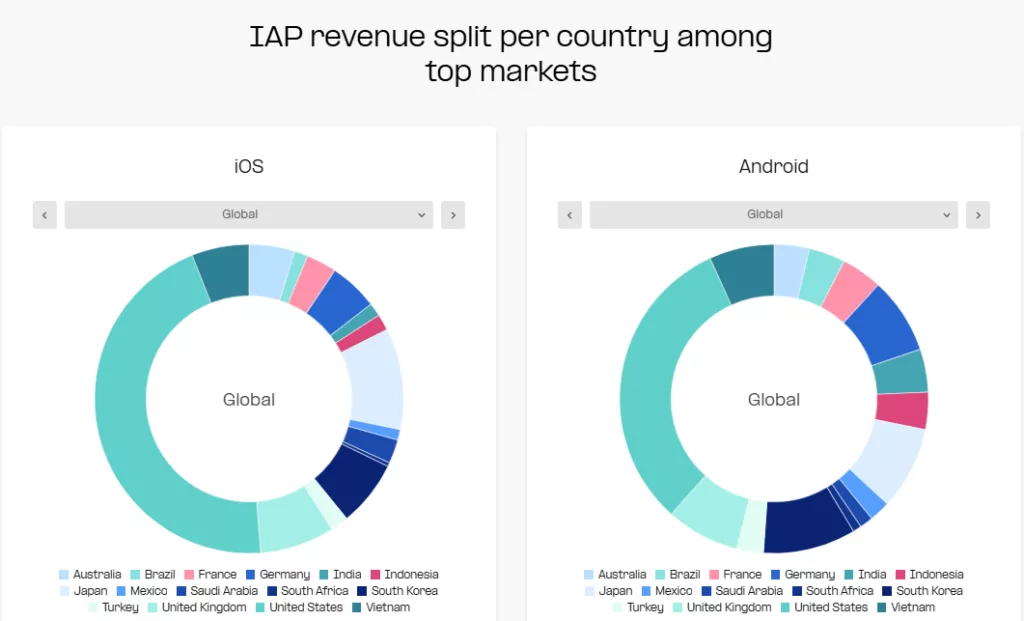

- The Revenue Fortresses (The West): The US and Western Europe remain the heavyweights. Western markets dominate In-App Purchase (IAP) behavior, generating 66% of global iOS revenue [2]. The US alone commanding 45% of all iOS spend [4]. Data confirms that Tier-1 Western countries remain the primary growth engines for casual genres, with the UK and US showing +28% and +10% year-over-year revenue increases in the Puzzle market, respectively [2].

- The Growth Hot Zones (Emerging Markets): While Western User Acquisition (UA) budgets tightened, emerging markets ignited. Turkey has firmly established itself as a mobile power player, seeing a 25% rise in In-App Advertising (IAA) revenue and becoming a central hub for hybrid-casual development. [5]

- The Volume Engines: Nigeria and Kenya are driving install scale, with Nigeria leading regional growth at 11.2% [5]. Meanwhile, China-based publishers have aggressively expanded westward, commanding a massive share of global UA spend to export top-grossing Strategy hits like Last War: Survival.

These insights reveal a fundamental industry shift: relying solely on saturated Western markets is no longer a guaranteed path to profitability. To thrive, companies must adopt a bifurcated strategy. They need to maximize long-term retention and direct-to-consumer monetization in Western ‘Fortresses,’ while heavily investing in emerging ‘Hot Zones’ (like Turkey) and volume drivers (like Nigeria) for scalable acquisition. With Chinese publishers also expanding aggressively westward, diversifying your media mix and geographical targeting is essential to defend traditional market dominance

2. The Genre Wars: “Cozy” Mobile vs. “Hardcore” PC

Gaming Devices Trends

Player motivations have diverged significantly by platform, forcing designers to tailor mechanics to specific psychological needs.

Mobile: The “Cozy” Revolution

US and European players increasingly cite “stress relief” as their primary motivation. According to global surveys, 77% of players use video games to help them feel less stressed, and 70% rely on them to feel less anxious [6]. This psychological driver has fueled a surge in the Puzzle and Simulation genres. (Methodology Note: These findings are based on a large-scale global study of active video game players ages 16 and older. It surveyed representative demographics across multiple regions, including 1,554 respondents in the UK and 1,006 in Spain, analyzing the impact of gaming on mental resilience, cognitive skill-building, and community connection [6].)

- Puzzle: Now the #1 genre in the US by reach. Within this category, low-stress “Block Puzzles” saw a staggering 911% revenue increase, jumping from $15.4 million to $156 million year-over-year [4].

- Strategy Surge: Globally, Strategy games—led by titles like Whiteout Survival—became the top-grossing category. Based on the data we collected, this category saw a massive influx of player spending, earning an impressive $10.6 billion in H1 2025 alone [5].

PC & Console: The Return to Depth

Conversely, PC players are rewarding high-fidelity complexity and indie innovation.

- The Indie Takeover: Independent games accounted for 25% of Steam’s gross revenue in 2025 [5]. Viral hits like Lethal Company and Balatro proved that gameplay loops outrank graphical fidelity.

- The Chinese AAA Wave: The record-breaking success of Black Myth: Wukong (reportedly selling nearly 30 million copies [5]) marked Game Science’s arrival as a premium PC developer. This release single-handedly drove massive spikes in PC market expansion and shifted major segments of Steam’s gross revenue toward Chinese developer hubs.

3. Popularity by Continent: 2025 Leaders

Gaming Genres Trends

The table below highlights how cultural and economic factors shape regional gaming preferences. Mature Western markets predictably favor ‘cozy,’ casual experiences like Monopoly GO! and Royal Match for stress relief. Conversely, LATAM and MENA players increasingly prefer highly social, competitive titles (Free Fire, Whiteout Survival) for community building, while Asia remains a stronghold for deep, mastery-driven RPGs. This divergence proves that a one-size-fits-all global strategy is obsolete; publishers must localize core gameplay loops to match specific regional psychological drivers

| Continent | Lead Game / Genre | Primary Motivation |

|---|---|---|

| North America | Roblox / Monopoly GO! | Socializing & Stress Relief |

| Europe | EA Sports FC 26 / Royal Match | Competition & Relaxation |

| Asia | Honor of Kings / Genshin Impact | Mastery & Collection |

| LATAM | Free Fire | Social Interaction |

| MENA | TopTop Lite / Whiteout Survival | Community & Strategy |

4. Monetization: The “Direct-to-Consumer” Shift

Gaming Monetization Trends

2025 was the year developers declared independence from the 30% “App Store Tax.” To protect margins, the top 100 grossing games aggressively adopted Direct-to-Consumer (D2C) web stores, with revenue from these channels reportedly growing 46% year-over-year. This was driven by “Web Shop exclusive” offers that grant players 20–30% more currency for the same price [4].

Casual games like Match Masters also adopted “Build Your Own Bundle” mechanics. This allows players to “pick their price,” a psychological shift that significantly boosted conversion rates in a high-inflation economy.

Strategic Outlook for 2026

Gaming expectations this year

The industry has moved from a “Hit-Driven” business to a “LiveOps-Driven” business. With Casino revenue declining (-7.5%) [4] and Hypercasual pivoting to Hybrid models, the winners of 2025 were those who could retain users for years, not days.

This LiveOps approach is heavily visible in console-to-mobile strategies; following the findings we got regarding EA’s FC Companion app, “Shared systems and interfaces keep activity continuous, reducing churn and ensuring every new launch inherits an already engaged player base.”(7)

For 2026, the mandate is clear: diversify or die. Publishers relying solely on the Apple/Google duopoly are seeing margins erode, while those building diversified web funnels and cross-platform ecosystems are capturing the next wave of growth.

Discussing this shift, Q1 market reports highlight the new reality of user acquisition: “Marketers are increasingly building multi-partner strategies that balance scale, intent, and efficiency, rather than relying on any single network to do everything” [3].

Final Thoughts: Navigating the 2026 Gaming Landscape

As the gaming industry shifts from a growth-at-all-costs mindset to a precision-and-retention model, winning the battle for attention demands a nuanced approach to player psychology and platform dynamics. To thrive, companies should focus on four key strategies:

Balance the Reach vs. Revenue Divide: Embrace a dual-platform strategy. Leverage Android for broad reach and volume, while aggressively expanding your media mix to capture the concentrated revenue growth on iOS, where competition is fiercest (1) (2).

Prioritize Retention Over Acquisition: With user acquisition costs climbing, prioritizing remarketing, VIP access, and owned-media flows yields far greater margins—especially during highly competitive commercial quarters (3) (4).

Elevate AI to Strategic Intelligence: Move beyond using AI just to scale creative output. Advanced teams are shifting from basic AI reporting to using it to interpret market fluctuations and inform long-term LiveOps and monetization decisions (5).

Deep-Localize for “Hot Zones”: As Western markets saturate, entering emerging volume drivers (like Turkey, Nigeria, and LATAM) requires more than language translation. Core gameplay loops must be localized to match specific regional psychological drivers.

Ultimately, the winners of 2026 will be those who abandon a one-size-fits-all approach. By aligning deep product experiences with specific user expectations, publishers can build resilient ecosystems that retain players for years to come.

——————————————————————————–

Sources: [1] Newzoo Global Games Market Report November 2025 Update [2] State of gaming marketing in 2026: Trends, AI & growth challenges [3] Singular Quarterly Report (2026 Q1) [4] AppMagic Monetization Report 2025 [5] Aream & Co. Video Game Market Update (Q4 2025) [6] ESA Power of Play Global Survey 2025 (7) 2025 Cross-Platform Gaming Report